demand

- asset types

- money

- currency: coins, bills

- deposit accounts: bank deposits

- bonds: interest rate, not used for transactions

- money

- money vs bonds dependent on…

- level of transactions: need money on hand to avoid having to sell bonds, dependent on spending per month etc

- interest rate on bonds: holding wealth in bonds is for interest, hassle of managing bonds is dependent on rate

- money market funds pool funds of many people to buy bonds

- terms

- income: earning from work + interest, dividends; flow over time

- saving: after-tax income not spent

- wealth: value of all financial assets minus financial liabilities

- investment: purchase of new capital goods

derivation

- : amount of money people want to hold

- if nominal income increase, transactions increase proportional, increase proportional

- based on some function of interest rate,

- has negative relationship with

determining interest rate

-

focus on supply of money and equilibrium

-

in real world, two types of money: deposit accounts supplied by banks, currency supplied by central bank

-

assume deposit accounts do not exist, only money is currency

-

suppose central bank decides to supply money equal to , thus , for supply

-

equilibrium requires money supply equals demand, that

- so and

- shows that must be such that for given income people must be willing to hold money equal to existing money supply ; called the relationship

- i.e. increase to supply of money by central bank leads to decrease in interest rate

- decrease in interest rate leads to increased demand for money, so it equals increased money supply

open market operations

- central banks change supply of money by buying or selling bonds

- central banks wants increase, buys bond and pays for them by creating money; if wants to decrease, sells bonds and removes from circulation money in exchange for bonds

- called open market operations as they happen in ‘open market’ for bonds

- expansionary open market operation → expands supply of money

- contractionary open market operation → contracts supply of money

bond prices and yields

- suppose one-year bonds with payment of and some price ; interest rate given as

- price today from one-year bond paying year from today is

- central bank buys bonds → supply of bonds decreases (less fulfilled demand) → price increases → interest rate goes down

- central bank sells bonds → supply of bonds increases (more fulfilled demand) → price decreases → interest rate goes up

liquidity trap

- assume central bank could always affect interest rate by changing money supply

- however, interest rate cannot fall below zero

- as interest rate decreases, people want to hold more money + less bonds

- as interest rate becomes zero, people want to hold money equal to , i.e. right when it hit

adding deposit accounts

assets/liabilities

- central bank

- assets: bonds

- liabilities: central bank money (reserves + currency)

- banks

- assets: reserves, loans, bonds

- liabilities: deposit accounts

cont

- up to this point, assuming only currency supplied by central banks

- banks keep as reserves some funds they receive

-

- on given day some depositors withdraw, other deposit cash; no reason for inflows and outflows to be equal

-

- on given day, people with accounts write checks to other people with accounts; what bank owes to other banks can be larger or smaller than what is owed to it

-

- there are certain reserve requirements applied in areas (europe in this case, with a reserve ratio of 2% on certain deposit types

-

- loans represent most of banks’ non-reserve assets, bonds account for the rest

- bonds/loans are approximately equivalent in the model

- assume only reserves and bonds as assets

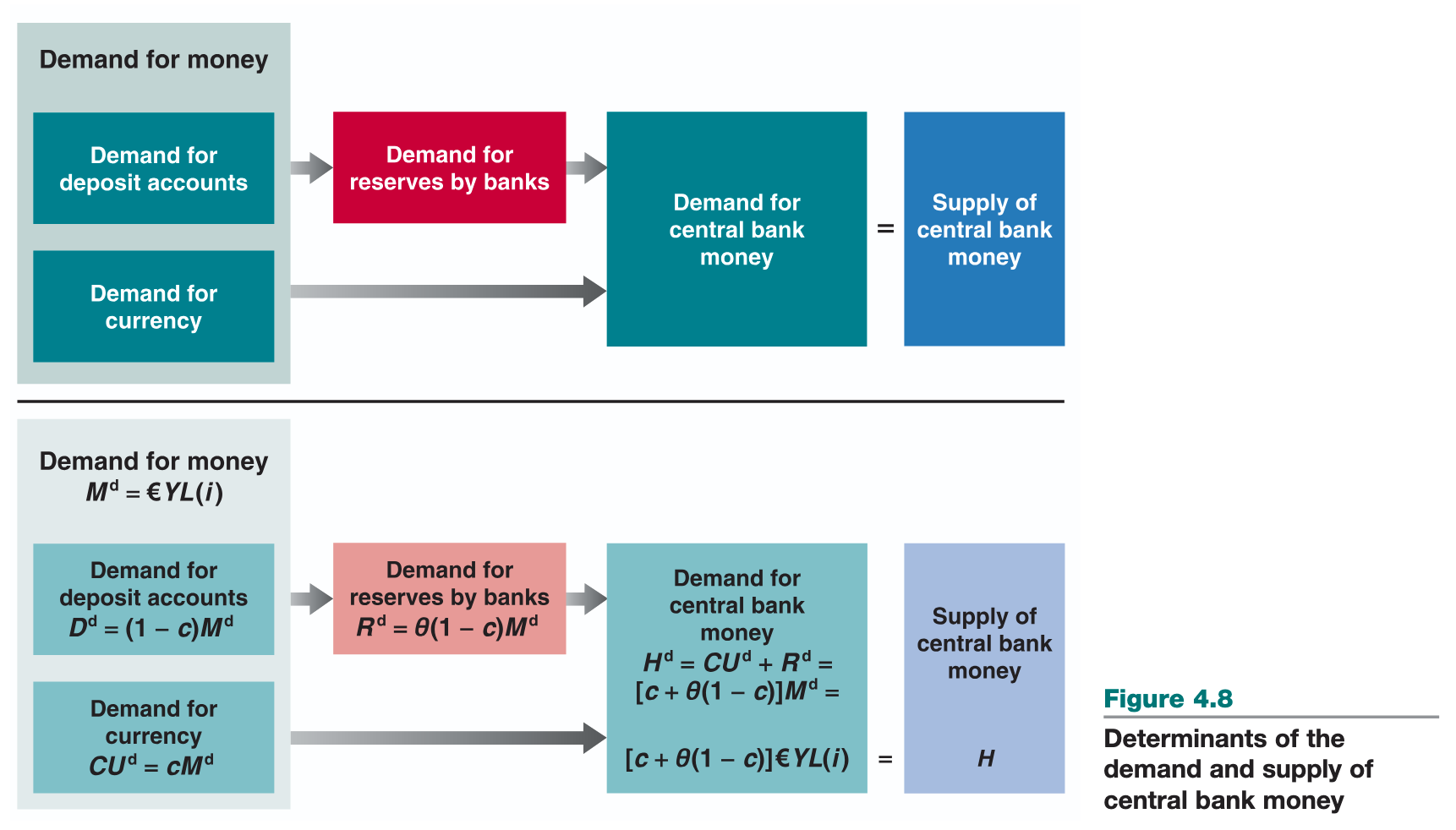

- demand for money

- what determines the demand for deposit accounts vs currency?

- in the equations, the vs factors, where is towards demand for currency

- what determines the demand for reserves by banks?

- based on the amount required by the country, e.g. 2%, and , the demand for deposit accounts

- what determines the demand for central bank money?

- based on a negative relationship with a function of interest

- how does the condition that demand/supply of central money be equal determine interest rate

- the demand is through , so if and are set, has to follow through